- 01- Markets discount recessions; certainty fades.

- 02- Food inflation lags energy; shocks hit CPI later.

- 03- Food risk underpriced; six-month lead to CPI.

The Honda Prelude

I joined The BIP Show this week to talk through how I am thinking about markets when certainty disappears and narratives start doing the heavy lifting. It is a useful companion to this note and sets the frame for what follows. Listen here.

TLDR: markets are discounting machines that look across the recessional valley.

I also run through the list of attendees for Read Corporate’s Resources Rising Stars event which I will be attending in Adelaide week after next. Click here to attend.

Food Before Fuel

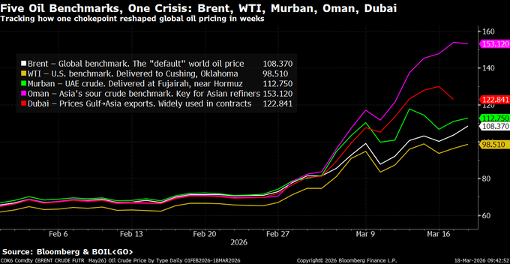

Oil is shouting. Funnily enough it’s shouting different volumes depending on where you happen to be listening.

There’s more to oil than WTI and Brent.

and...

So, when someone says “oil is x” then your response should be “where?” because we’re all learning this month that oil markets are smooth, fungible market right up until the time something goes wrong.

After that it’s every man for themselves. We’re all finding out that there’s a shortage of oil at $80/bbl but a wonderful supply at $180/bbl.

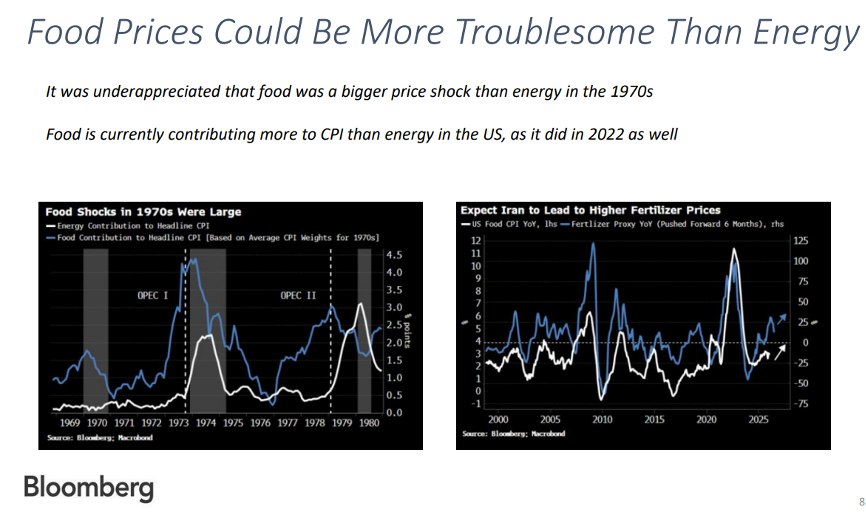

But the most useful insight I heard this week had very little to do with crude. It came from Simon White of Bloomberg on MacroVoices, and it was about food.

Simon’s point was simple and uncomfortable. In past commodity-driven inflation episodes, food ended up doing more damage than energy. It arrived later, embedded more deeply, and proved far harder to reverse once it took hold.

Energy shocks grab attention. Food shocks change behaviour.

His chart deck shows that food’s contribution to CPI overtook energy at key moments in the last cycle, including 2022, and that markets consistently underprice food risk because they are distracted by oil prices.

That matters now, because the early conditions look uncomfortably familiar. It usually takes about six months to kick in.

I’m not sure how adding 25bps to older Australians’ bank savings rates is meant to help this but I don’t work at the RBA so who am I to opine?

Why Food Inflation Works on a Delay

Food inflation does not show up when the shock happens. It shows up when the buffers run out.

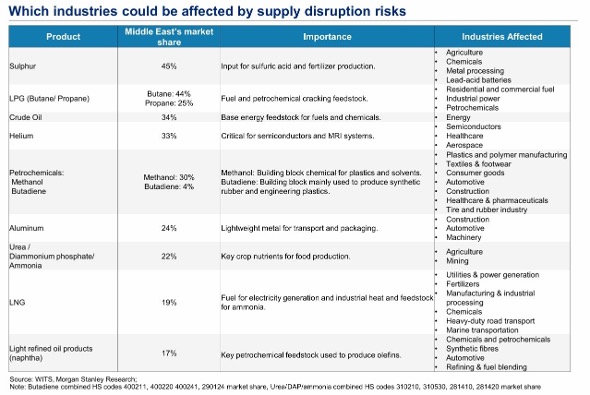

Above: The inputs…

Below: the buffers…

Agriculture works on long lead times. Inputs are ordered months in advance. Crops are planted seasons ahead. Contracts, storage and logistics absorb stress quietly until the next reset point.

That delay is why food inflation repeatedly catches policymakers and investors on the back foot.

Farmers have already planned and ordered fertiliser for this season. In many cases it is already delivered or contractually locked in. That makes some of the more breathless commentary about immediate shortages or instant price spikes overstated in the near term.

But that does not weaken the signal. It strengthens it.

The real impact shows up in the next ordering cycle. When fertiliser, transport, energy, and financing costs are reset together. That typically takes around six months. Food inflation arrives late, then refuses to leave.

What the Tweets are Actually Telling us

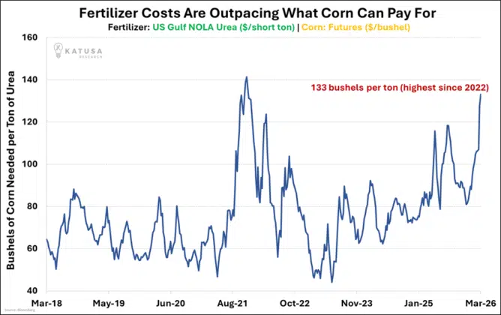

This post from Katusa Research highlights growing stress in agricultural inputs and upstream supply chains, particularly fertiliser availability and cost pressures. The implication is higher unit costs feeding into food production as contracts roll and inventories turn over.

“About 50% of the nitrogen applied to U.S. corn goes in during spring planting. A vessel loaded in the Persian Gulf today takes 30 days to reach a U.S. port And another 3 to 4 weeks to reach interior farm markets. The American Farm Bureau Federation sent an urgent letter to the White House on March 9th. And their message was direct: fertilizer is stranded in the Middle East during the most critical window of the agricultural calendar.”

This follow-up post from shanaka86 explains the lag. Input shocks do not move straight to supermarket shelves. They move through inventories, processing, logistics and contracts first, then hit retail prices in a concentrated wave.

Put together, these are not calls for an immediate food crisis. They are warnings about timing.

The system absorbs pressure quietly, then passes it on all at once. That is exactly how food inflation becomes both persistent and politically toxic.

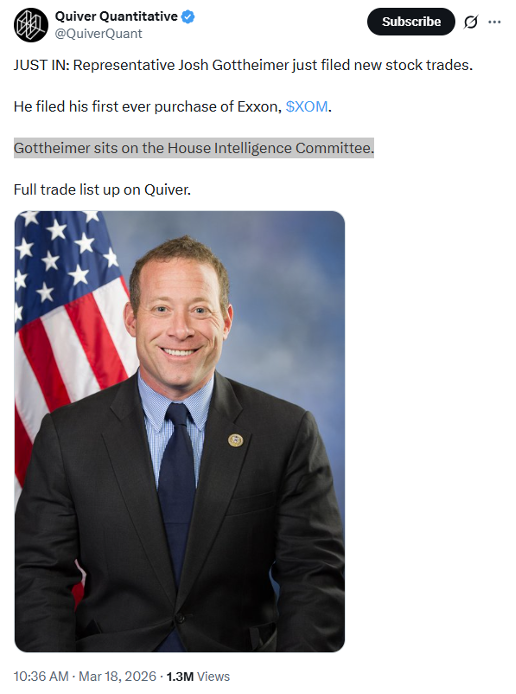

Follow the Money

If you want to know whether this matters yet, stop watching CPI prints and start watching Members of Congress trades.

Yeah, they’re not opening the Strait any time soon…

Play the Tape to the End

(...in which I make the boldest forecast since 2020.)

Ok so here’s how it all transpires:

Global shortages and supply chain issues. People physically can’t get the goods or can’t afford them even if they can see them. Food is the main driver of this lunacy.

It’s like Covid again but without the stupid elbow handshake. I’ve said that numerous times.

The world simply stops moving for a while. Flights grounded, spending goes to necessities.

Then come the rate cuts. To zero. Again, same as Covid.

Gold absolutely ramps. $5k will seem like nothing.

Markets, now able to see the other side of the recessional valley, have their best six month run since the sugar hit in 2020.

If your broker calls, answer the phone. If they’re bearish, hang up.

Credit Should Be Front-Page News

Before everyone goes back to arguing about inflation prints, there is a far more important signal that deserves attention.

This screenshot shared by Negligible Cap shows JPMorgan and Goldman Sachs offering hedge funds a way to short private credit using baskets of listed companies with exposure to the space.

Banks do not build products like this casually. It’s actually quite scary in many ways.

The time will soon be upon us to make some very drastic cuts and more drastic long term decisions.

Make your shopping lists now on stocks to buy and be prepared to get very greedy.

Get the wire before the market opens.

The ASX small-cap stories that matter, filed before 9am AEST. Curated by the Small Caps desk.